Your credit report could have mistakes, but here's how to fix it and improve your score

Errors on your credit report could be dragging down your score and costing you financial opportunities.

Your score affects whether you can borrow money — and how much you'll pay — to borrow money, so you want it to be accurate. But one common cause of a lower score could be no fault of your own.

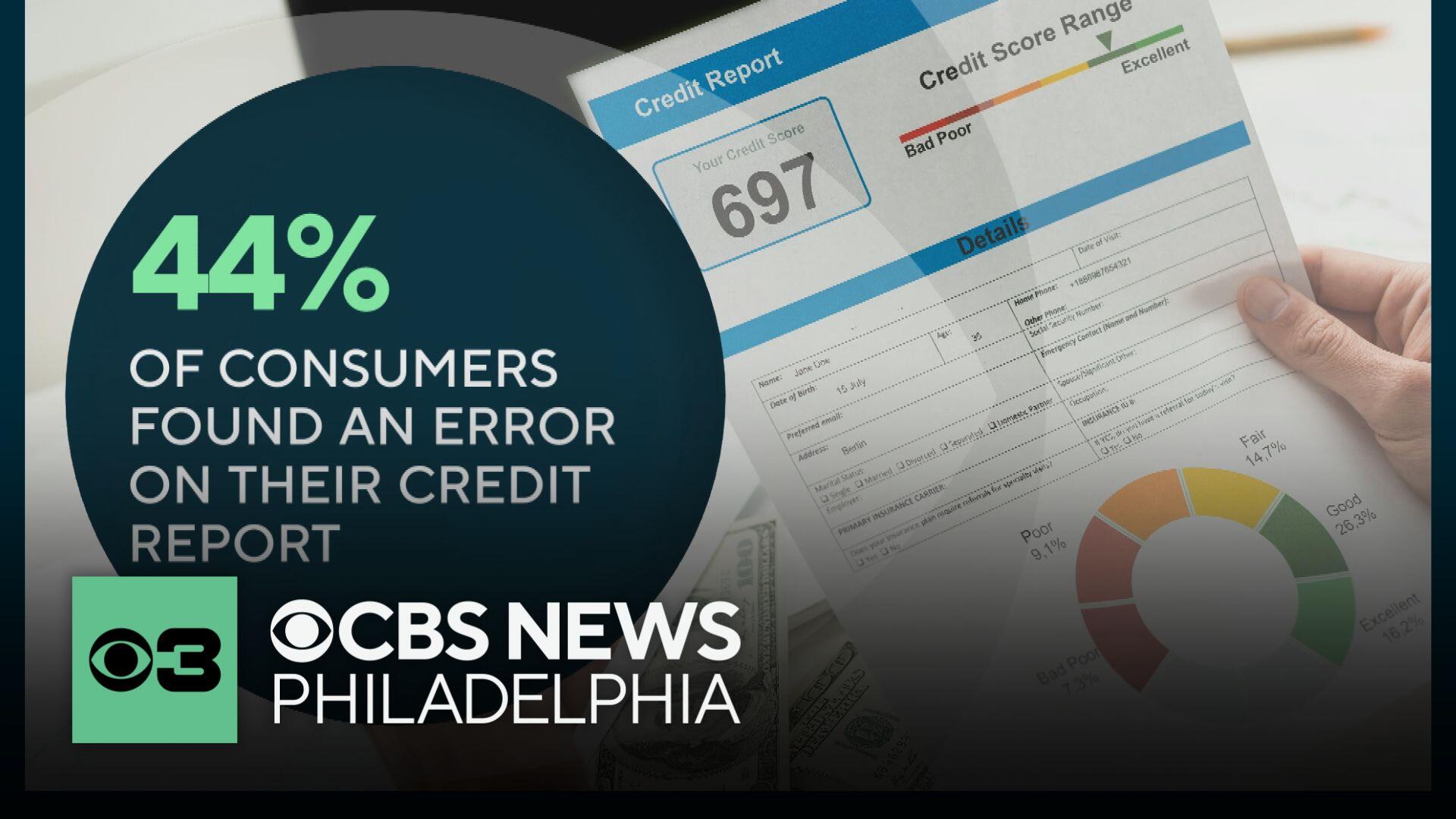

Almost half of consumers who volunteered to check their credit reports found mistakes in them, according to Consumer Reports. But you have the right to dispute errors in your report, and you can do it for free.

Types of errors

Errors can range from simple misspellings to serious instances of someone else's debt showing up on your credit report, according to consumer attorney Bob Cocco, who specializes in credit report disputes.

In other instances, Cocco said a creditor might provide incorrect payment history, balance information or payment status, like reporting a closed account as open, an incorrect date of late payment, or listing the same debt more than once.

A mixed file, where your information is mixed with someone else's, is another common error.

"For example, if you have a twin, you both have the same last name and you have the same birthday, that's enough sometimes to get you confused. If you're a senior and a junior, your dad has the same name, that could also lead to a mixed file error," Cocco said.

Millions of Americans every year are impacted by identity theft, which can also result in credit report errors.

Disputing the mistake

Consumers have the right to dispute any information they think is wrong on their credit report.

If you identify an error on your credit report, you should start by disputing it with the credit reporting bureau, like Experian, Equifax, or TransUnion.

You can dispute the error online. Experian, Equifax and TransUnion all allow you to submit a dispute through an online portal.

But attorney Bob Cocco recommends sending your dispute letter by certified mail and asking for a return receipt, so that you have a record that your letter was received. You can also attach copies of supporting documentation, which is critical.

"That is the most effective, and the reason is that you can monitor whether it's been received by sending it certified mail, and you can also specify in the letter what evidence you're attaching to prove why the information that you're disputing is inaccurate," he said.

"I help people all the time write these letters for free. You want to tell the credit reporting agency what's wrong and what you want to do to correct it."

You can use a sample dispute letter like this one from the Federal Trade Commission as a guide.

Credit bureaus must investigate your claim and make any necessary updates to your information within 30 days, according to the FTC. Credit bureaus also must contact the company that provided the information. If the company finds the information was inaccurate, they must notify all three credit bureaus to correct your file.

If you suspect that the error on your report is a result of identity theft, visit IdentityTheft.gov to generate documentation you will need when working with the credit bureaus.

Protecting your credit

One way to ensure you're able to address errors quickly is to regularly review all three credit reports.

By law, you are entitled to one free copy of your credit report every year, but Experian, Equifax and TransUnion now allow you to get your credit report for free every week.

You can access your credit report through AnnualCreditReport.com.

Credit repair scams are also common, the FTC warns. Be suspicious of any company promising to remove all negative information from your report. While there are ways to fix mistakes on your credit report, you can't legally remove information that's correct and up to date.

If you're considering paying a credit repair company to help fix your credit, the FTC says to remember that anything they advertise they can do for you legally, you can do yourself for little to no cost.