After scammer moves $1,500 out of couple's savings account, bank denies their fraud claim six times

It's not always a bad thing when the spouse keeps tabs on the other's spending, because for David McCarty, his wife's vigilance might've saved them a fortune.

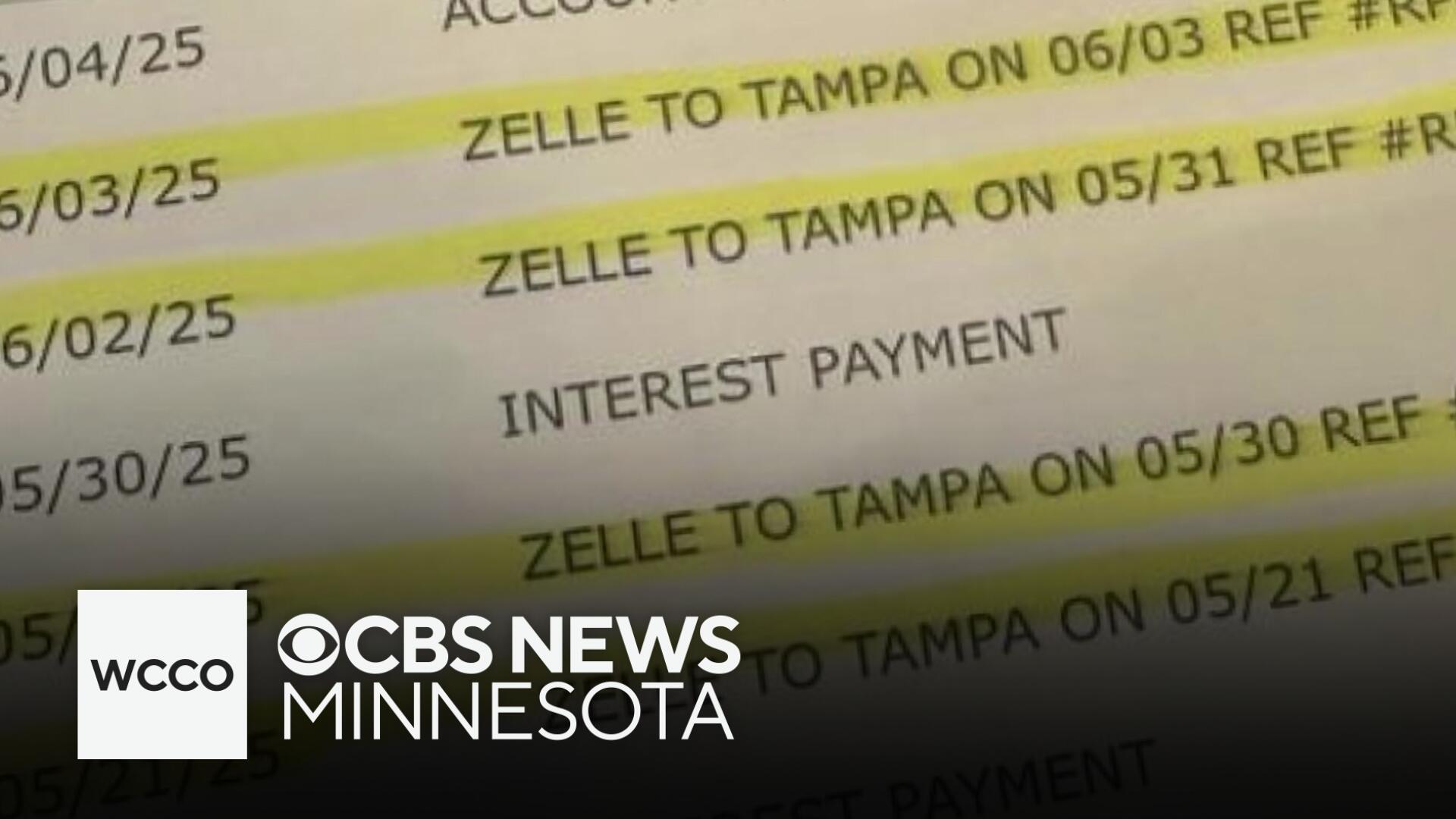

"She just happened to look at the savings account, which should have no activity," McCarty explained. "She said, 'Dave, have you been transferring money using Zelle to Tampa, Florida?'"

The answer was an emphatic "no", but the McCartys' account showed four transfers over several days totaling more than $1,500. When McCarty called Wells Fargo to alert them to the fraud, they found another red flag: the scammer changed the phone number and email address attached to the account.

"We talked to customer service and they wouldn't talk to us without us telling them what our email was, and they said it was wrong," he recalled. "Finally, we talked long enough and we gave them our social security number and they agreed to talk with us, and that's when we were able to shut things down."

Filing the claim then proved to be an even more aggravating experience: according to McCarty, Wells Fargo denied the claim six times.

"They kept coming back and telling me (I) authorized it or authorized someone else, and we said, 'There's no way. We don't know anyone in Tampa.' I wasn't given the trust of being a longtime customer and I was being accused of fraud myself."

The experience, while frustrating, also proved revealing in that it showed the difference in consumer protections for bank accounts versus credit cards.

"We've had fraud on our credit card, and they call us and we get the money reimbursed," McCarty noted. "Here, Wells Fargo didn't catch this. I want people to be aware that you're not protected for your checking and savings accounts."

Indeed, credit cards often provide zero liability for fraudulent transactions, as well as notifications for unusual activity. Banks, however, generally require the customer to manually set up those alerts. Protectons are also stronger for credit cards because transactions are more directly linked with the card issuer's payouts, whereas bank accounts are the sole responsibility of the account holder.

After more appeals, McCarty did eventually get his money back, and a spokesperson for Wells Fargo told WCCO News McCarty's experience "does not reflect" the standard of service the bank wishes to provide.

"We are pleased to have resolved this matter for our customer. At the same time, we sincerely apologize for the inconvenience and worry they experienced during the time it took to complete the resolution process," the spokesman wrorte. "This does not reflect the level of service we aim to deliver. We remain committed to protecting our customers and stopping criminals from engaging in fraudulent activities. We continue to invest in customer education, employee training and advanced technology to help detect and prevent fraud and scams."

Wells Fargo also shared its online security center for customers to become more familiar with potential scams and ways to avoid them. Wells Fargo also posts a Security Brochure with other information to help account holders.